He doesn't seem to "get it" that he is being used by this Tory-led government to justify an infamous double whammy of massive increases in pension contributions at the same time as equally massive cuts in pension benefits.

There is no repeat no dire crisis in funding arrangements for public sector pension funds. There are indeed problems but remember only 4 years ago there was a huge row between the then Government and the public sector unions about pensions. A tough compromise deal was eventually hammered out which saw rises in employee contributions, reductions in benefits and caps on employer (taxpayer) contributions. Which the unions accepted despite the pain because it was promised that this will make the schemes affordable and sustainable. So what on earth has really changed in these 4 short years about pension fundiamentals?

What is happening is quite simply a Thatcherite and Orange book ideological attack on the principal of collective provision coupled with plain old fashioned public spending cuts. For example this government has reduced grants to Councils by £1 billion based on an assumption that staff contributions to their pension schemes will go up by some 50%! (repeat 50%). If this goes ahead then this will mean that pensions will become unaffordable and people will leave their schemes in droves. If this happens and members can't afford to remain or join then yes, the public sector schemes will indeed fail.

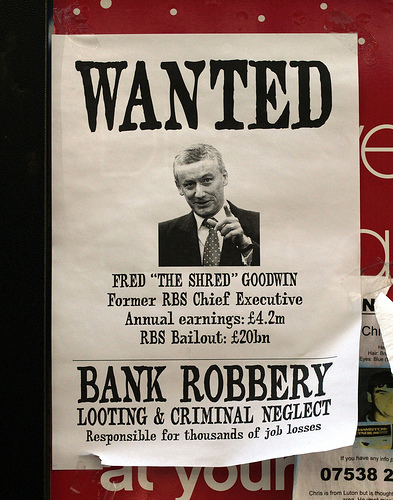

So yet again we have some of the most low paid and vulnerable in our society being expected to help make good a public spending deficit caused solely by Bankers and the Rich who ripped off this country and now expect us to pay for it.

This lunchtime I was interviewed by Channel 5 News (who reported only my comments on the likelihood of strike action), live on Sky News (robust but interesting) and ITN (see caption and this link).